Financial Management

Click wheel to review standards

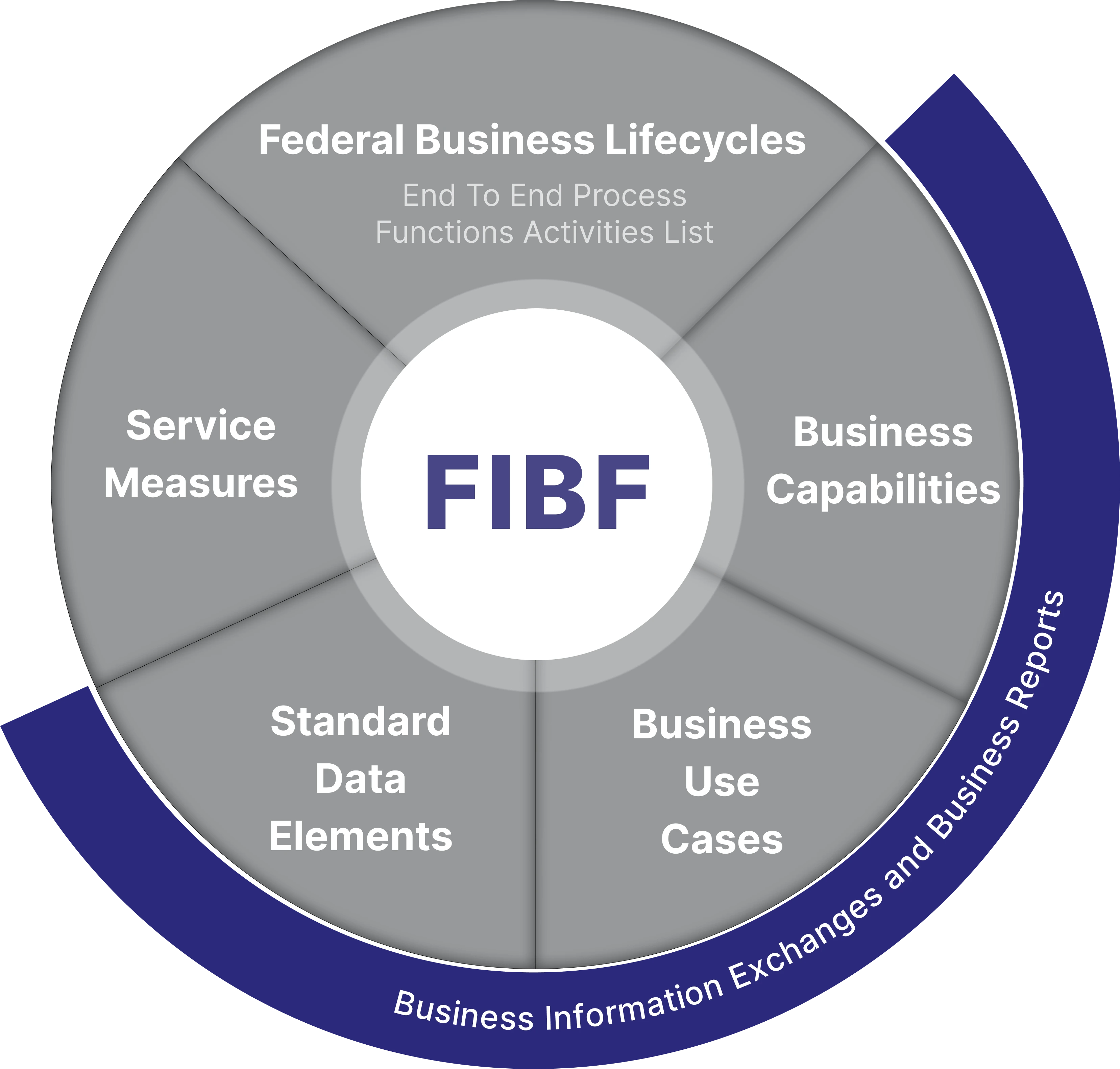

Federal Integrated Business Framework (FIBF)

The FIBF is a model that enables the Federal government to better coordinate and document common business needs across agencies and focus on outcomes, data, processes and performance. It is the essential first step towards standards that will drive economies of scale and leverage the government’s buying power.

Core Financial Management Solutions (Core FS) Pre-Built Business Information Exchanges (BIEs) - date posted 11/15/2024

Core Financial Management Solutions (Core FS) Pre-Built Business Reports - date posted 11/15/2024

Financial Management Standards Lead

Name: Treasury, Bureau of the Fiscal Service

Website: Financial Management Standards | TFX: Treasury Financial Experience

Contact: FMLoB@fiscal.treasury.gov

Download Financial Management Business Standards Components

Federal Business Lifecycle - Financial Management

Federal Business Lifecycles, functional areas, functions, and activities serve as the basis for a common understanding of what services agencies need and solutions should offer.

Functions: Breakdown of a functional area into categories of services provided to customers.

Activities: Within a function, processes that provide identifiable outputs/outcomes to customers are defined as activities.

Select from the list of available functions to view associated activities

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

| Identifier | Activity | Description |

|---|

Business Capabilities - Financial Management

Business Capabilities are the outcome-based business needs mapped to Federal government authoritative references, forms, and data standards.

| Capability ID | Function | Activity Name | Input/ Output/ Process |

Business Capability Statement | Authoritative Reference |

|---|

Business Use Cases - Financial Management

A set of agency “stories” that document the key activities, inputs, outputs, and other LOB intersections to describe how the Federal government operates.

Standard Data Elements - Financial Management

Identify the minimum data fields required to support the inputs and outputs noted in the use cases and capabilities.

Service Measures - Financial Management

Define how the government measures successful delivery of outcomes based on timeliness, efficiency, and accuracy targets.

Business Information Exchange and Business Reports - Financial Management

Business Exchange and Information Reports outline the critical data interactions and communication flows between systems and stakeholders supporting Financial Management in the Federal government.

Core Financial Management Solutions (Core FS) Pre-Built Business Information Exchanges (BIEs) - date posted 11/15/2024

Core Financial Management Solutions (Core FS) Pre-Built Business Reports - date posted 11/15/2024